Strategic Outlook: India Bilateral Trade Agreement – India & United States

Posted On : Wed Feb 04 2026

The recent announcement of a bilateral trade agreement between the US and India marks a pivotal shift for domestic markets. Under the new framework, the US will reduce reciprocal tariffs from 50% to 18%positioning India competitively against Asian peers while India moves toward zero-tariff barriers (specifics pending). We view this as a major catalyst for Indian equities, driven by: a) a potential reversal in Foreign Portfolio Investor (FPI) outflows, a primary market overhang for 15 months, and b) an estimated 50–80 bps boost to nominal GDP growth alongside INR appreciation. Our March 2027 Nifty 50 target is 29,500 (20x FY28E EPS). Key overweight sectors include Financials, Capital Goods, Defense, and Consumer Discretionary.

Trade Mechanics and Energy Shifts: The US tariff reduction to 18% is accompanied by India’s commitment to eliminate non-tariff barriers. Notably, India plans to pivot energy sourcing from Russia toward the US and Venezuela, with a long-term objective of importing over USD 500bn in US goods a significant scale-up from the current sub-USD 50bn annual run rate.

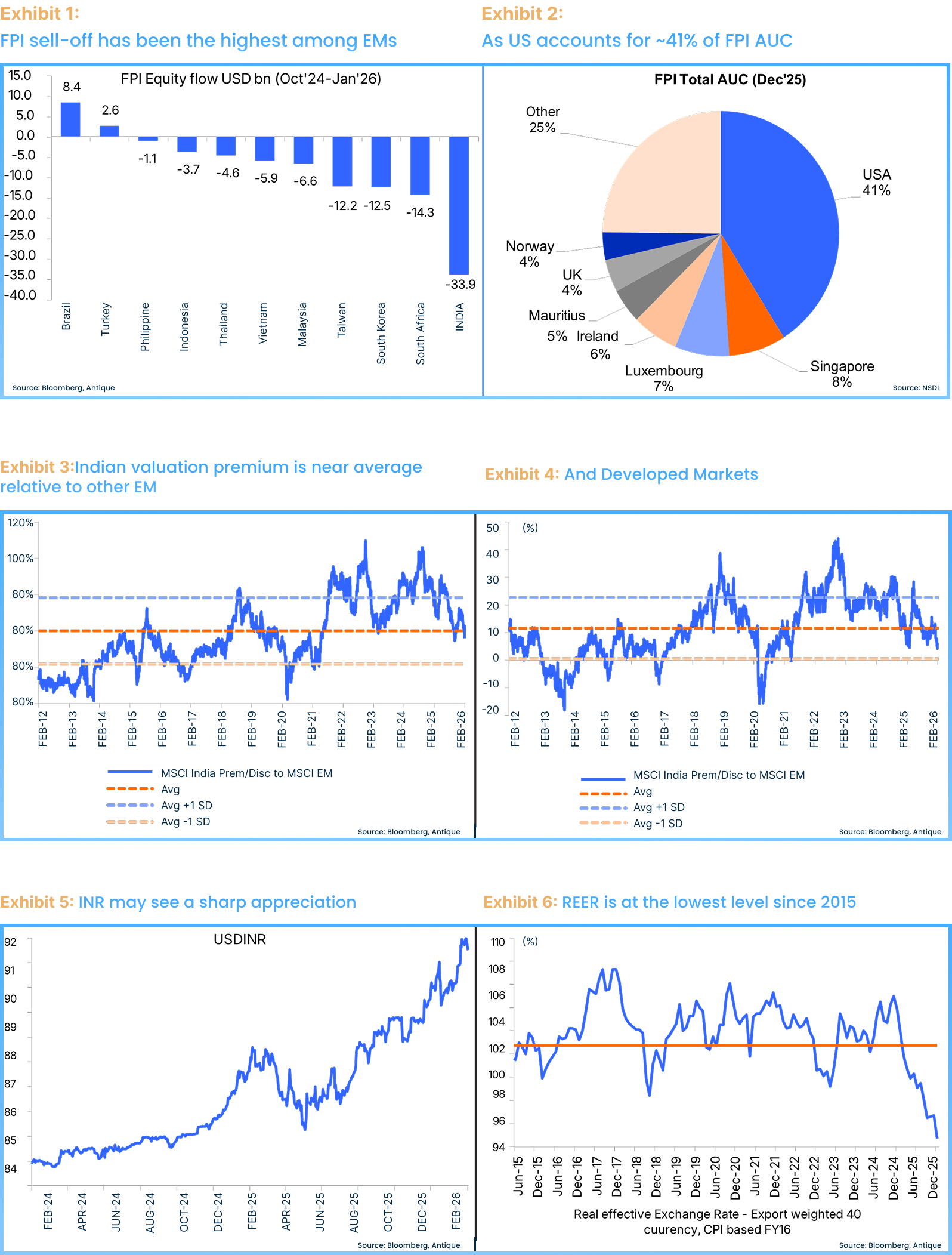

FPI Flow Reversal: Since October 2024, India witnessed record EM outflows of USD 34bn. Given that US-based capital represents ~41% of FPI Assets Under Custody (AUC) and valuation premiums have moderated to long-term averages, we anticipate a sharp trend reversal. Primary beneficiaries include high-FPI-concentration sectors (Real Estate, Telecom, Healthcare) and sectors currently under-owned relative to historical benchmarks (Capital Goods, IT Services, Financials).

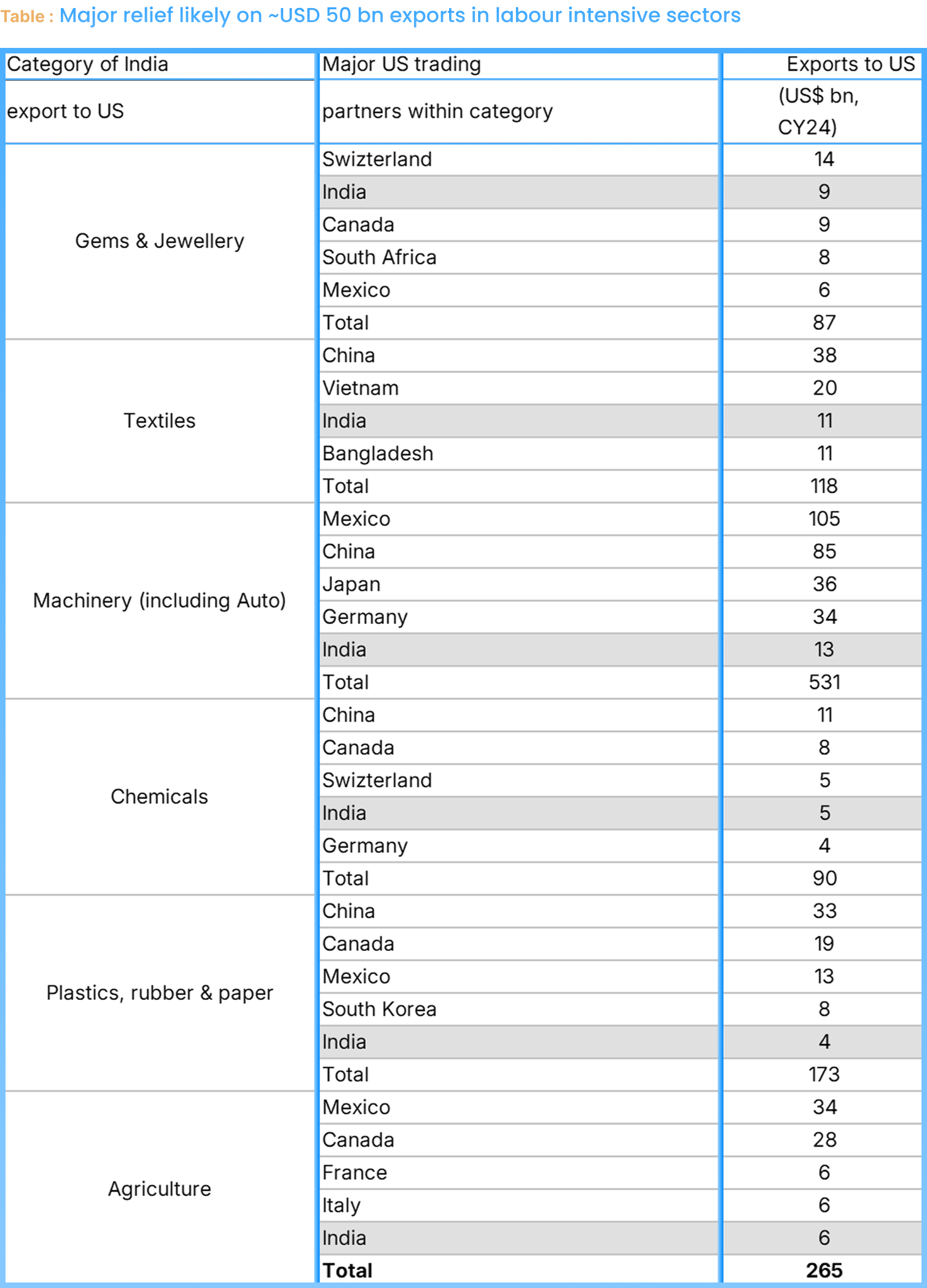

Macroeconomic Impact: The 50% tariff regime threatened ~USD 50bn in exports (1.2% of GDP). Relief in labor-intensive segments specifically Gems & Jewelry (USD 9bn), Textiles (USD 11bn), and Machinery (USD 13bn) is expected to add 50–80 bps to GDP. Stronger capital inflows and robust domestic macros should support the INR, particularly as the Real Effective Exchange Rate (REER) sits near decade-lows.

Sectoral Positioning: We expect an immediate re-rating for sectors previously constrained by trade friction, including Banking, Pharma, and Industrials (Power T&D, Cables). Our portfolio remains structurally bullish on India, maintaining an overweight stance on Financials, Capital Goods, Defense, and Consumer Discretionary to capture this fundamental tailwind.

The recent U.S.-India trade deal marks a significant shift in relations.

Below is a concise summary

The Current Deal & Immediate Impact

A Necessary "Floor": The previous situation was unsustainable; a deal was essential to prevent a total collapse of U.S.-India relations.

The 18% Tariff: While 18% is high by historical standards, it is a "smooth landing" compared to the threatened 50% rate.

Competitive Advantage: India now holds a slight edge over competitors, as ASEAN nations are mostly at 19% and Vietnam is at 20%.

Diplomatic Success: U.S. Ambassador Sergio Gor is credited with resetting the tone and moving the relationship "downfield."

Strategic Concerns & Risks

The "Tariff President": President Trump views tariffs as a tool for more than just trade—using them to influence drug policy, foreign alliances, and supply chain choices.

China’s Shadow: China doesn't need to match India’s rate; it only needs to get close enough to complicate "China plus one" manufacturing strategies.

Unrealistic Targets: The goal of India purchasing $500 billion from the U.S. is viewed as a "stretch," given that current exports are only around $83 billion.

The Long-Term "Trust Gap"

Politicization: The relationship, which had been depoliticized since the 2000s, has become political again due to the volatility of the last six months.

Dangerous Precedents: Tying trade penalties (like the 25% oil penalty) to third-country relationships (e.g., Russia) sets a negative precedent for future diplomacy.

Erosion of Trust: Trust is much easier to lose than to build; while the deal is a "win," the underlying ceiling of trust between the two nations may have been lowered.

Bottom Line: India and the U.S. should take the win, but remain cautious. The "fairy dust" has settled, but the collateral damage to the partnership remains.

Disclaimer

This document has been prepared by Waya Financial Technologies Pvt. Ltd. and is provided to you for information only. This document does not constitute a prospectus, offer, invitation or solicitation and is not intended to provide the sole basis for any evaluation of the investment product or any other matters discussed in this document. This document is made available to you because Waya believes that you have sufficient knowledge, experience and/or professional advice to understand and make your own independent evaluation of the risks and rewards of the investments and/or other matters discussed in this document and to make your own independent decision whether to implement the same. Any view expressed in the document is generic and not a personal recommendation and/or advice. It does not consider your risk tolerance, financial situation, knowledge and experience. Please discuss with your investment advisor if you seek advice on whether the proposed investment product is appropriate for you. The investments discussed in this document may not be suitable for all investors. Investments are subject to market risk. There can be no assurance or guarantee that any investment will achieve any specific return. Unless expressly stated, product performances are not guaranteed by Waya or their affiliates or any government entity. Past performance figures are not verified by SEBI. Past performance is not necessarily an indicator of future performance. Actual results may vary significantly from the forward-looking statements contained in this presentation due to various risks and uncertainties, including the effect of economic and political conditions in India and outside India, volatility in interest rates and the securities market, new regulations and government policies that may impact the business of Waya as well as its ability to implement the strategy. The information contained in this document has been obtained from sources that Waya believes are reliable, but Waya does not represent or warrant that it is accurate or complete, and such information may be incomplete or condensed. Neither Waya, nor any affiliate, nor any of their respective officers, directors, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any upon this document or its contents, or for any omission. The views in this document are generally those of Waya and are subject to change without notice, and Waya has no obligation to update its views or the information in this document. Waya or its affiliates may have acted upon or have made use of material in this document prior to its publication. Waya does not provide legal or tax advice and should you deem it necessary to obtain such advice, you should approach independent professional tax or legal advisors to obtain the same. This document is confidential and may not be reproduced or disclosed (in whole or part) to any other person without our prior written permission. The manner of distribution of this document and the availability of the products may be restricted by law or regulation in certain countries and persons who come into possession of this document are required to inform themselves of and observe such restrictions. This document is not directed to, nor intended for distribution or use by, any person or entity in any jurisdiction or country where the publication or availability of this document or such distribution or use would be contrary to local law or regulation, including for the avoidance of doubt the US. The contents of this document have not been reviewed by any regulatory authority in India or in any other jurisdiction. If you have any doubt about any of the contents of this document, you should obtain independent professional advice. The name of the strategy does not in any manner indicate the quality of the strategy, its future prospects or returns. The product strategies mentioned in the document may change depending upon the market conditions and the same may not be relevant in future. The sector(s)/stock(s)/issuer(s) mentioned in this document do not constitute any recommendation of the same and the strategy may or may not have any future position in these sector(s)/stock(s)/issuer(s).

Regards

Amit Vora, CEO